The title of this post can be read two ways. As parents age, they become more anxious, but we adult children become more apprehensive, too. Like a migraine headache, financial security just keeps pounding away. Especially when bills like the one above arrive. Dad came out one morning unable to speak clearly, having experienced what we later learned was a TIA or mini-stroke.

My Dad was unusual for recognizing his increasing limitations as he had plenty of medical reason to expect that a period of incapacitation could precede his death. He had a will, gave one of my brothers financial power of attorney, had a checking account with two of us on it in addition to himself, turned over bill-paying to us, and purchased long term care insurance (though, regrettably, without an inflation rider making those years of premium payments a ridiculously bad investment).

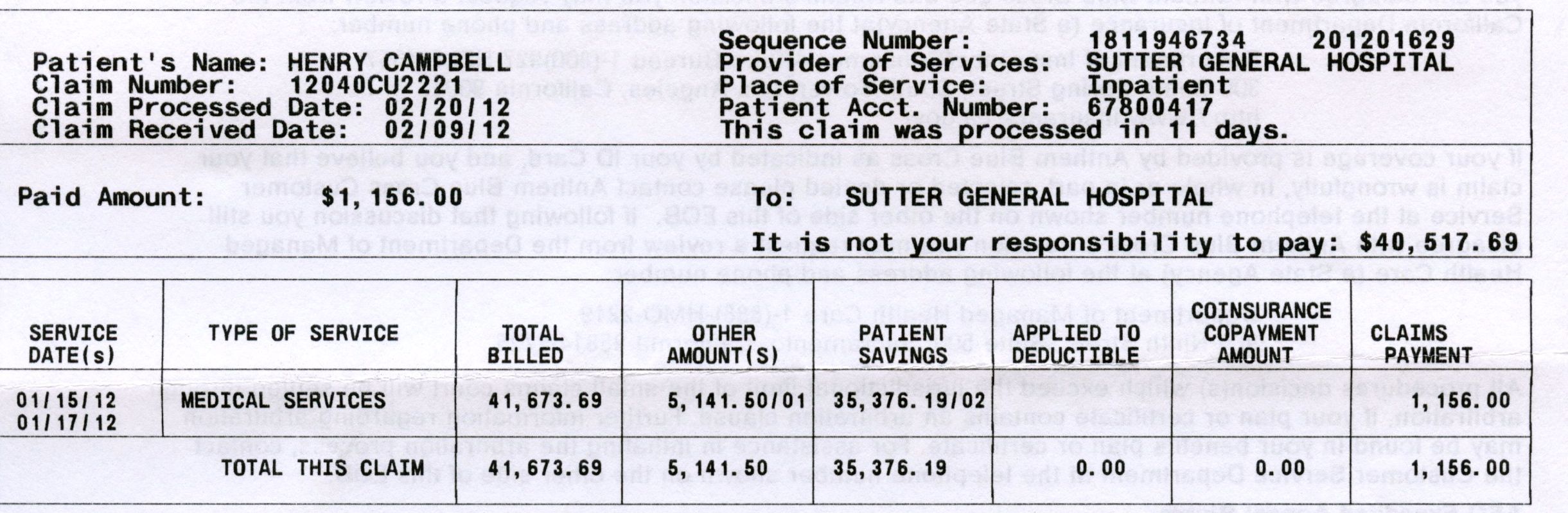

That said, he constantly worried about whether his financial resources were adequate. Anytime an “Explanation of Benefits” arrived from his supplemental Medicare plan insurer, it set off a new round of questions – even if it clearly stated that he did not have to pay the amount. I took to carrying with me a handwritten ledger of his monthly income and monthly obligations.

“See? You’re fine,” I would reassure him.

The flip side of the parent-adult child financial anxiety coin is harder to solve. How do you have “the talk” with a parent who doesn’t think his or her financial situation is an appropriate topic of conversation? At a financial seminar hosted by UBS last week, I learned that the average age of a widow is 55. Older married women – still – don’t necessarily know the details of their financial accounts.

This morning’s New York Times carries a great article, “The Talk You Didn’t Have With Your Parents Could Cost You.” Among other tips, it quotes Amy Goyer, a caregiving expert at AARP, who offered these practical suggestions:

- Know what type of information you are seeking before you start a conversation, such as: whether a will exists, a financial power of attorney, a medical power of attorney or health care directive; what their health insurance covers, including long term care insurance; whether they have life insurance; and if there is a list of every singe account they owe or collect money from.

- Start conversations with an “I” statement such as, “I’m concerned about doing the right thing when you pass.”

Although my Dad shied away from the Internet (after a few attempts), the article also reminds adult children to secure passwords for any Internet-only accounts. And the worst place to keep legal documents and instructions, the article suggests, is a safe deposit box, because survivors often lack access to them.

I know it’s “nature’s way,” but certain aspects of aging have always struck me as cruel; high among them, our parents’ feeling of insecurity as they lose ground. Though adult children have a moral obligation to protect aging parents’ security, we can’t lose sight of the need to ease their hearts and minds. That often takes finesse, driven by caring concern.